If you hate discussing money, do yourself a favor and skip this long post.

As I mentioned, 2013 is different because Dustin and I are combining finances for the first time. We've been living together for 7 years, married for 1.5 and I guess we're ready. Sharing money is a big step for me. I've been working in some capacity since high school and I love having my own money. Those numbers in the bank feel like tangible security to me.

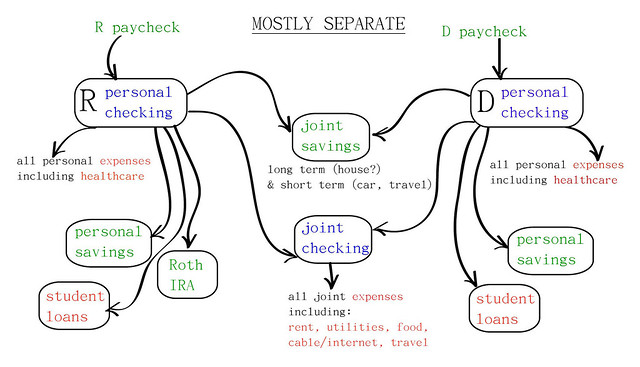

Prior to marriage (and for 1.5 years after) we'd shared a joint checking and savings account and had a joint credit card. Once a month we both deposited equal amounts of money in the joint checking account, transferred equal amounts of money to the joint savings account and then all our joint expenses went on our credit card and got paid from our joint account. It worked perfectly, partly because we both earn exactly the same amount of money and so we didn't have the awkward situation where one person has more disposable income than the other.

Our sharing but separate set up worked great, but it started to get more complicated once we got married. Both our healthcare costs started coming out of my pre-tax paycheck, which means I was suddenly taking home slightly less and this seemed like a good time to transition (obviously we could have easily remedied this by having D reimburse me or contribute more to our joint account but we both felt ready). If either of us wants/needs to change jobs in the future, we should feel supported and pooling our money is a good way for us to get to that place. At this point it's more of a mental shift than anything, because we do still earn roughly the same amount of money.

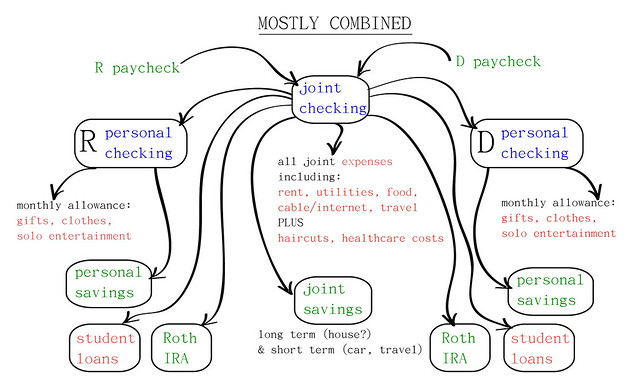

In February we started depositing our paychecks in our joint account, then transferring a monthly allowance to our individual accounts. I'll still have my personal retirement account and we'll still have personal savings along with joint savings. Almost all our expenses will go on the joint card but our allowances will be dedicated for clothes, times when we go out solo, gifts, etc. We aren't ditching our personal cards because they carry credit history but also because we both appreciate having some personal space. I have no issue with the fact that my favorite lip gloss costs $20 and I have weeks where I buy two cookies a day at Tavern but I like pretending I have a thin veil of privacy because no one else sees my statements. D has similar issues with shoes, I think. I don't know. That's the point of the cards. Anyways, the idea is that as long as our personal spending fits in with our joint goals, it's no one's business where the allowance goes.

Annoying logistics:

We didn't even have to set up new bank accounts and this was still a huge pain. I sat down with a spreadsheet and wrote down all our balances (checking, savings, credit cards, student loans, retirement) for both our joint and individual accounts. I wanted to start from zero so I figured out what we each needed to contribute to pay off our credit card statements (we don't carry a balance on any of our cards, so we zero it out each month) and how much we needed to have in our personal accounts to avoid fees. Previously this hadn't been an issue because I'd had direct deposit going to my personal account and if you do that most banks will waive a monthly service charge without requiring a minimum balance. We transferred money from our savings accounts to make sure we had more than enough in both our personal and joint accounts because we weren't sure how long it would take for re-routing to take place. Then we re-routed our automatic withdrawals for our student loans and retirements to our joint account. I re-routed my direct deposit to our joint account.

We're checking everything carefully for a couple months to make sure it all worked. So far one of my student loans re-directed successfully but the other didn't (bizarrely, they are serviced by the same company) so I had to pay it manually.

loved this! thanks for the insight..

ReplyDeleteDude, those student loan websites are terrible! I set up payments for a couple weeks later, and then student loan company seems to forget about the payment! Craziness!

ReplyDeleteYou'd think they'd want your money, right? I can't figure out why it's always so complicated.

Deletethis is so helpful, thank you! my husband and i are just about to combine all of our finances and i was feeling overwhelmed. hearing how/what you did helped the process seem a bit more doable.

ReplyDeleteI'm glad it helped! I was a little overwhelmed as well, which is why it took me so long to transition. But really, it isn't all that hard. You just have to figure out what you feel comfortable with and discuss it together. It might not look exactly like ours, because everyone has a slightly different system. It's funny how what works for one person is not at all what works for another.

DeleteThis is so interesting. I love reading these posts. Keep them coming!

ReplyDeleteLove the illustrations -- this sounds exactly like the switch we made two years ago. Transferring the student loan electronic debits was definitely the biggest pain, but since then, it's all been smooth and I'm very happy with the system. For us, the no-questions asked personal allowances are key, and the whole system has helped us really get our joint savings in gear. Hope it works well for you!

ReplyDeleteThis is exactly how we did it/do it - both the before and the now. Too funny.

ReplyDeleteI really enjoy hearing about your budgeting. Although I'm not living with my bf and we are not married yet, it's really interesting to hear what I should be doing in the future!

ReplyDeleteI reread the previous budgeting post, and I actually do something similar to the punchcards myself, except electronically. I use an app called Spend Free. Basically, I type in my monthly allowance each month for expenses I can control (aka not rent or utilities, etc.) and every time I buy something, I deduct the amount I spent from it. I don't like to keep receipts either (unless it's something I might return, like you), so I just input the amounts soon after the purchase. Since it's on my phone, which I almost always have on me, it's super quick.

Oooh - I'm curious! I'll have to look up that app. So far, the major downside to the punch card system is that so many places no longer keep actual pens by the check out area! I guess I knew that we'd mostly switched to electronic signatures but hadn't really thought about it. It means I have to keep a receipt tucked behind my credit card until I have a chance to enter it. Not a big deal, but an app might be nice.

DeleteI feel like we're budgeting kindred spirits. I love a good budget and I think sometimes my friends think I'm crazy for it. My fiance and I currently do the way you and D have been doing it... it's working for now, but I can see how it might not work forever.

ReplyDeletewe do something very similar to this, although all of our savings accounts are joint. sharing money is HARD. we've been doing it since we got married (3.5 years ago), and i still feel like i'm in the process of transitioning. since joe makes significantly more money than i do, there's no way i couldn't live without my own checking account. i'm all for both of us contributing to our living expenses, but having him pay for my clothes and makeup still (and probably always will) feels off to me.

ReplyDeleteI can see where you're coming from, but part of the reason he makes more than you is because you take care of Cheech, right? In my area that would cost $1600 a month if you paid someone else to do it. That's a huge contribution just in financial terms (not even going into all the other benefits).

DeleteMoney is so tricky because we all have really different emotional reactions to it. I was really embarrassed to have to admit that D that I just didn't want to combine retirement accounts, ever. I'm proud of the money I've saved and even though I assume we'll be spending it together at some point in the future, I still want it to be mine. Not logical, just emotional. But still valid.

it's funny, the idea of combining retirement accounts never occurred to me - and we have zero other individual accounts (we combined checking accounts about a year after moving in together and have had all subsequent paychecks in all subsequent jobs - and decades! - deposited straight into the common one; we also randomly grab money out of each other's wallets and pockets, as does the cat). i've had a 401k through my company for most of that time and joe's had a thrift savings plan rolled over through his various government jobs, so it's gone, literally, without saying.

DeleteLMO, ours was a little strange because I have a substantial (compared to my income) retirement account and D didn't have one set up. We could maximize our tax benefits by jointly contributing to my work retirement account which would be in my name but would essentially be joint. However, I just wanted to keep my account separate, for no rational reason. So instead we opened up a separate account for D and now we each contribute separately. In fairness to D, I agonized over this a bit and when I finally brought it up he thought it was a total non-issue and thought I was weird for worrying about it.

DeleteI also have a tendency to get scrooge-y about some expenses and then overly sensitive about others. It's an unfortunate quality but it appears to be innate. Hence, our need for some separate spending money.

that seems perfectly reasonable to me. our full disclosure system, in turn, works out for me because i can very easily spend money on very weird shit; knowing that joe knows how much i pay for it makes me think twice, at least.

Deletegood for you for having a substantial retirement account! i didn't look into setting one up until my little sister started shaming me about it.

I'm with Lauren. The sharing of a retirement account is news to me. I've had a Roth since I was 18 but have never had a retirement account through a job. MAS on the other hand has only had a retirement account through his job. About three years ago we started a Roth for him and also additional (separate) investment accounts.

DeleteWe only started sharing a bank account about a year ago (we've now been married for 5 and living together for ... um ... 10?) and that was mostly due to the fact that I took a break from getting paid in any consistent way and him transferring money into my account was making me feel weird. Also I am responsible for our financial anything and that sometimes made a monthly transfer tricky when our electric bill fluctuates by upwards of $300 depending on the time of year. Now we both put whatever we make into our joint. He takes what he needs for student loans and everything else gets paid from our joint. I have my own account but don't use it much. We do have separate credit cards.

I like this post! Money is funny and it's nice to see that others think that too.

I don't think combining retirement accounts is typical at all (and we didn't end up doing it) but it was something that was on the table for us, just because of our situation. But it's funny that no one combines them, even people who have almost everything else combined! I wonder why that is.

DeleteYour reason for combining is exactly why we felt we should move in that direction. I know it would feel weird for one of us to get an allowance from the other person but it doesn't feel so weird to get an allowance from the joint account. It doesn't make any difference at this point, since we're both working, but who knows where we'll be in five years?

great tips!!

ReplyDeleteYour first set up is exactly my husband and I's set up and we are thinking about depositing our entire paychecks into the joint account, but I do still want to keep my personal checking for the same reason! I like my $20 Sephora products and I'm sure my husband won't quite get it.

ReplyDeleteGreat post!

I love these posts, being in a similar position—my husband and I have been using the mostly separate system (and giving the punch cards a try...very useful since neither of us are very good at keep track!) but it's nice to have ideas on how we could transition eventually.

ReplyDeleteThe diagrams are perfect! I love that you both have a personal allowance and personal savings whilst having everything else combined. Must share with J and see if we can work this all out a little more cleanly like you guys have.

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteI do love me a flow chart! My husband and I have been idly discussing combining finances since we got married, but we've never pulled the trigger, mostly out of laziness. We can't come to a consensus about keeping personal accounts or just using credit cards or just checking the joint account balance frequently. Reading about how you and other couples are doing it is really getting me thinking. Thanks so much for following up on the budgeting post with this!

ReplyDeletegreat post lady! moved in with my bf recently and now we're engaged so will be looking into this for future reference. Thanks, E

ReplyDeleteThis is a fantastic post! Me and my boy are debating the same issue. However for us, it gets tricky with student loans... Mine will be forgiven thru a public service forgiveness program and he owes a small fortune. AH. Being an adult can be so complicated.

ReplyDeletex

This is a personal decision, of course, but we decided not to worry about evening out the student loans. I've been paying mine off for 8 years and I have made big inroads whereas D only started paying his recently and has a much higher interest rate to boot. We decided that our student loan debt would just be considered joint debt and we're paying them from our joint account.

DeleteMerging debt is a big deal, though, so it definitely gets tricky!

This is the dilemma of all of my current couple friends and I so I appreciate you sharing. We're currently on the first step - separate bank accounts with a joint checking for wedding expenses but once Andy graduates law school I think we will take the leap and have a joint everything. Have a great weekend! xx- Mallory

ReplyDeleteThanks so much for writing about this. It's so important but it's something that a lot of people seem to avoid talking about. I'm about to move in with my boyfriend, and while we're still awhile away from sharing finances, it's definitely something that's been in the back of my mind on the "some day we're going to have to figure this out" list. Cheers!

ReplyDeleteWhile I am not married, (dating nearly 8.5 years!), this is the type of thing that causes me much anxiety. I'm very proud of my healthy savings account and the thought of SHARING what I've worked hard to maintain. Reading this has definitely eased my mind a little. It's possible and not as scary as my brain makes it out to be..or is it?! Yikes!

ReplyDeleteIt is a little scary and I wouldn't push yourself! We were both at the point where we felt comfortable combining. If you aren't comfortable yet, figure out a system that works for you guys! Money is tough because we all are coming from different places and have different emotional responses to it.

DeleteThis is such a great post! Getting married in September and the conversation keeps getting swept under the rug by us both. My fiance makes about tripple what I do, but currently we split all our expenses 50/50....groceries, rent, utilities. Obviously for me it is much more of my income than for him. I think he is hesitant to share but I am also a better saver with my retirement funds. I have almost as much as him and have been saving half as long! If anything, I am going to use the flow chart to get is talking so THANK YOU!!

ReplyDelete