I seem to have finally hit on the one method that works for both of us because our budget cards were a total success last year (printable versions shared in this post). Except for a short period of time in December when I attempted to hide from the cards because we were in the midst of moving + the holidays and all we were doing was eating out and then going to Ikea to buy things and also drinking more than usual in a vain attempt to make ourselves believe that packing and unpacking boxes could be fun. That was a dark couple of weeks.

We're continuing with the cards this year because they work and I don't have a better idea. I try not to draw attention to them in real life because they make me feel like a dorky third grader. Our friends who are aware of them have teased us a little this year but when I check out our results I feel completely vindicated.

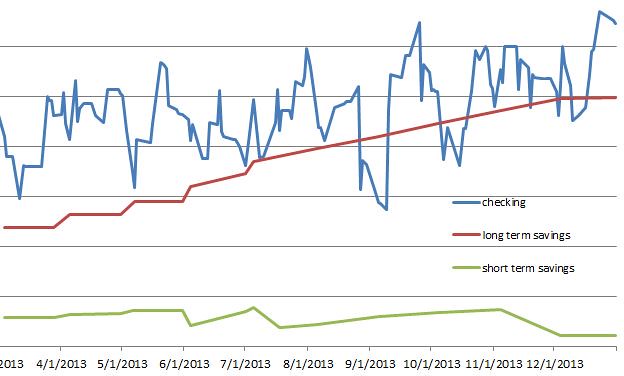

{budget trending}

We didn't touch our long term savings despite some temptation. That depressing dip in September was when we were hit with two expensive car repairs within a few weeks of our scheduled vacation. I wish I could bill the city of LA for potholes, but apparently when you hit one and manage to jam your braking system it is your fault because a pothole is considered a stationary object. True, but somehow it seems unfair. Our short term savings (car repairs, vacations, etc) never got up any steam but our other accounts are headed in the right direction.

I've rejiggered our budget for the coming year to account for changed circumstances. Downsizing to a smaller place gave us some breathing room, some of which will be set aside for Circe. This was the main reason we decided to find a less expensive apartment. Circe is generally healthy but having a dog inevitably means vet bills (or, at a minimum, purchasing dog food and weird anxiety reducing shirts). We set up a savings account that's earmarked for pet expenses and automatically deposit $100 a month. Of course, one serious vet visit can wipe out a year's worth of savings, but at least we'll be cushioned a little for the routine stuff.

I also gave us a little more spending money and increased our short term savings contributions. I clearly hadn't put enough in short term savings last year because we were constantly wiping it out and it was becoming clear that at that level we'd never be able to go on vacation again. I made (very) small increases to our retirement and long term savings. I try to follow the balanced money formula to preserve our quality of life and that means no more than 50% on needs, up to 30% (and no less than 20%) on wants and at least 20% on savings. Our current budget stands at 43/26/30. Depending on how you categorize things I might be overestimating our savings. I lump our student loan payments into savings when I suppose you could call them a need. You have no idea how rich we'll feel when we're finally done paying off student loans. Having the percentages to aim for has been hugely helpful to me when writing our budgets. Left to my own devices I tend to feel guilty about spending money but having a sanctioned 20 - 30% for spending makes it easier for me to justify. Sure, we could save way more if we cut it out but my goal isn't to be filthy rich at 70 years old while having denied us any vacations for 40 years. My goal is to win the lottery and stop budgeting, obviously.

Our first budgeted holiday season left us scrambling a little so for 2014 I set up yet another savings account* that's specifically for Thanksgiving + Christmas expenses. I based the goal amount on how much we spent this year, added a little extra and then broke it into monthly contributions. I'd originally just figured we could use our short term savings but HA! there was definitely no money in there after our unexpectedly expensive September. This extra account will make next year easier.

We're in kind of weird place financially. Not nearly enough savings to consider a house purchase, but enough that maybe we should do something other than let it sit in the bank? I think this year I might try to do some research and figure out what our strategy should be.

Disclaimer - As always, when talking about budgeting, I am fully aware of how lucky we are to be able to stress about self imposed limitations. Not having enough money to eat out as often as we'd like or buy as many nice clothes as we would like is hardly a reason to cue up the tiny violins. I admit that a certain amount of self pitying teeth gnashing sometimes occurs at the end of the month but it's the difference between eating boxed mac and cheese vs. eating Humboldt Fog, and neither one is the same as going hungry. We take our self imposed budget seriously, but knowing we have money in savings is what makes it possible to look at it as a game instead of a constant state of stress.

*All of our mini savings accounts are through CapitolOne, formerly ING. I like how easy it is to set up multiple accounts with automatic deposits and D and I can easily share access.

You could d a short term CD with your savings for now

ReplyDeleteI'll have to check the interest rates again - last time I was thinking about it, they just didn't seem high enough for it to be appealing to lock our money up, but I'm thinking they might be better now, right?

DeleteI tried your printable cards for a few months this past year and, while I thought they were awesome and the idea behind the categories totally worked for me, the physical card didn't so much because I was terrible about always having a pen and then terrible about remembering to add things. BUT I now do basically the same system using a free iPhone App called Goodbudget- it's worked really well so far!

ReplyDeleteI also can't recommend enough the book All Your Worth by Elizabeth Warren and her daughter- it was a quick read, and had great strategies for long term and short term savings... It's pretty amusing to read financial books written before 2007 and see the interest rates they quote- HAH!

I am going to check out that app! I love our system but the paper part is the downfall. We make it work because it's still better than any of the other systems we've tried, but I definitely would prefer an phone based system. If I knew more about coding I would totally make an app that did exactly the same thing and then we would be set.

DeleteThe app is amazing (at least so far- it's only been a month and half), but I wonder if it's wouldn't work for 2 people... maybe if only 1 of you added the grocery and communal money on yours...

DeleteHmmmm ... yes, ideally it would synch between the two of us. I'll check it out and see if it can do it!

DeleteWe've used goodbudget (formally known as EEBA, they also have a nice website and apps for all phone users) for years now. It does sync between people (multiple folks can use the same account). I can't reccomend it enough. And congrats with all your savings!

DeleteRachel, I find your posts about budgeting so inspiring!! I remember your first one a while back and always look forward to when you update. I grew up in the foster care system which meant financial education was always hard fought. Throughout the years, I have gone back to your posts for guidelines and good suggestions. Thank you for being open and honest about what it takes to make financial goals in your life happen!! I was so proud this year when I started really saving a substantial amount, 20% of my income. Given I am single, it's nice to reflect on your progress since I don't have a partner to confer with about said expenses. No one is going to chide me for buying that sweet jacket at James Perse, other than my own sense of responsibility. With that said, I have been struggling with what to do with my saved income as well. I heard putting it into a low risk mutual fund might earn about %6, which really adds up with compound interest over 1-4 years. I have my IRA Roth in Vangard (no fees) and was going to look there for an option. You might want to check it out. Really simple interface, again - little to no fees, and very well respect. Again, keep posting!! (I love your lifestyle posts, too) xo

ReplyDeleteI have my IRA Roth at Vanguard too! I've been really happy with it (um, not that I do anything other than automatically deposit money in it, but it seems good?).

DeletePart of my issue is not knowing when we'll need the money! I've been loath to make it untouchable on the off chance that we (magically) manage to figure out a way to buy a house. But, barring a lottery win, I think a down payment is out of reach so I should probably just suck it up and look at short term places where I can park it. Good thinking about checking Vanguard for other options!

I have my IRA with vanguard and finally created an account with them last year for some of my regular savings. I'm a conservative investor, and Vanguard funds are more of a risk than an online savings account with a locked in rate, so I only put in a small portion of my savings, but it's done really well this past year. I really wish I had done it years ago - it's just that no one told me this was an option. I thought mutual funds were just for retirement accounts.

DeleteAlso, I researched different online savings and CDs a year ago and decided on CIT bank. Their online savings account rate is around 1%, and then it's accessible, I can easily transfer money in or out. I used to have money in a CD, but now I'm nervous to have my money locked away, since we might decide to make a big life change in the next couple years.

I diligently track my own expenses, but now that I'm getting married I have to figure out how we can budget together since I know I can't get Evan to manually track expenses. Mint had some weird bugs when i tried it several years ago, but I guess I need to try it out again.

Okay, officially putting this on my list for the next month!

DeleteAnd ugh, figuring out a joint financial solution is such a pain. We all handle money and expense tracking so differently and finding a system that works well for two people is just plain difficult. All I can say is keep trying different systems until you find one that works! It's so hard to predict what will be good for both of you.

Thank you so much for your budget posts! I feel like budgeting is something that is so seldom talked about but is SO important. It's so nice to get insight into how other people handle this because I'm never quite sure if I'm doing it "right." I know someone just mentioned goodbudget (which I downloaded exactly 0.2 seconds ago), but also mint is a great free financial app for budgeting!

ReplyDeleteI've been so weird about Mint! Everyone loves it but I'm still a little nervous about giving any one website access to all my financials (and I know that so many people have reported on how safe it is and everything is online anyways, but I can't shake the irrational, freaked out feeling).

DeleteSeriously, YNAB is super great. The app means you enter transactions as you make them, which get matched later to the transactions from the bank (or you can enter them all by hand, but that's a lot more work!). We love it!

ReplyDeleteI've heard good things about YNAB! My only issue is that I don't love budget systems where I have to track absolutely everything (i.e. I'm not concerned with our gas or certain other categories) but there's probably a way around that if I looked into it!

DeleteThese posts are so reassuring to read. I love to hear how other people handle routine things. I'm a huge fan of both Elizabeth Warren financial principles and multiple savings accounts for specific things (I do miss the ING branding though...just me?). My mother also uses savings accounts this way and we recently figured out that it is a genetic trait: her mother does the EXACT SAME THING with envelopes in her sock drawer. VIrtual envelopes for the win!

ReplyDeleteNot just you! I really dislike the new branding. Ugh. Who would have thought we'd be so attached to orange and white?

DeleteFab, fab, fab! To this day I still cannot print the budget cards ... beginning to think there is something I am not doing right ... maybe they don't like English laptops? :)

ReplyDeleteOh, so sorry! I wish it wasn't being a pain for you! If you email me, I can send you the PDF directly. I have no idea why Google Drive can be glitchy but I haven't figured out a better way to post PDFs for download.

DeleteBudgeting – in my opinion, this is the common concern of most people. No one can blame you, right? It’s always an advantage to have money for any eventuality. So when unexpected things happen, your family is safe from the financial stress it might cause. Just like what you experienced with the accident. Thankfully nothing bad happened to you and your car has been taken care of. This may have been a disappointing moment but at least you learned a lot from it.

ReplyDeleteKayla @ GeorgetownShell.com

I always look forward to your budgeting posts! I do have a question about how you differentiate between short-term savings and long-term savings: is short-term vacations/presents/medical/etc and long-term retirement/future home purchase? Just curious.

ReplyDeleteAs far as your overall strategy, it sounds like you have been taking a page from LearnVest. I've recently really started to get into their program (not using their paid service). I highly recommend the CEO's new book - Financially Fearless. I've been giving copies to all my friends. Sounds like you've adopted those strategies already though. She recommends a 50/20/30 budget. The 50 is by far the hardest in the Bay Area, and I'm sure its the same down near you too. There's also an iphone app to track all transactions and budget by category and you can pull in all your accounts - bank, credit cards, IRA, 401k, etc. Much better than mint or other services I've seen.

That's basically it! Short term is both fun stuff and unexpected emergencies. We use it for travel and car repairs, usually. But we'll also use it if we have a big month and do a lot of entertaining at home (hosting can add up!) or if we have a month where we need to buy multiple wedding gifts, etc. (I'll try to work gifts and entertaining into our regular budget if possible, but I'm not averse to using short term savings if we get hit with several expenses at once). I also use a pre-tax health savings account for us, so our routine medical expenses mostly come out of that.

DeleteSo far, we're keeping our long term savings intact. The goals are fuzzy (house? hopefully?) but longer term than just a vacation. I'm hoping we won't have to buy another car for a long time, but if we did, I think it would come out of this fund. We also have retirement accounts, although we aren't funding them as aggressively as we would if we weren't also paying down student loans as fast as we can. So many competing needs!

I've never heard of LearnVest but I'll check it out! And ugh, hitting 50% is tough. Moving to a cheaper place (and sacrificing space) is the only thing that nudged us down. You can cut every category as much as possible but if your rent is high there just isn't that much wiggle room!

So excited for you guys that you get to have Circe full time! Have you considered pet insurance? I just signed up for Pet's Best (vet recommended) for my dog and it seems to be a good plan. It shouldn't cut into your monthly pet emergency budget too much, and it gives a sense of security that you might not have to empty out a years worth of savings for an unexpected illness or accident. It might not be for you, but worth a look maybe? Love your blog and I always look forward to your posts!

ReplyDeleteWe are so dorkily obsessed with her! We haven't really considered pet insurance (always assumed it was a scam?) but I might look into the plan you're using! Definitely worth a look, and running some numbers to see if our self insuring makes sense or if it's better to buy a policy. Thanks!

DeleteInfrequent commenter here. I really appreciate that you share your systems - menu planning, budgeting - with us.

ReplyDelete50/30/20 actually comes from Elizabeth Warren's book that she wrote with her daughter, Amelia Warren Tyagi. It's called All Your Worth. Learnvest doesn't give credit where it is due, so I like to mention that when it comes up!

We use ynab because it syncs amazingly well across our phones and computers. Its system is a little fussy if you have your own ideas about how you'd like to think about things, but it is so incredibly good for capturing our spending that we use it. The reports are also nice and you can export to .csv if you want to do your own analysis (though the exported requires a bit of tidying up).

I really enjoy your blog!

I think I need to read the Elizabeth Warren book! Always better to read straight from the source, I think, and the ratio has really helped me a lot with developing a budget. I'm also going to look into YNAB again, and see if it might work for us!

DeleteThe trick with ynab is that you don't need to use it the way they want you to. We are moving towards using their system because it does make sense, but initially we didn't. You can just use it as a tool to capture your spending by category and then copy what ever interests you into excel.

DeleteI also really like the 50/30/20 budget, it really helps you think straight!

In ynab, I made three major categories according to the 50/30/20 budget. When you go to reports you can see a pie chart (will a fancied up circle but it is a pie chart) by major category and it shows you what % of your spending went to each. So it becomes incredibly obvious if you are meeting the 50/30/20 goal. Doing that has made a huge difference to our thinking. You can drill down into each category in the reports but I love seeing the big picture so clearly.

I meant well up there but if I go edit the comment box will freeze :)

The econ major and nerd in me loves these posts so much! I used some of your tips from some of your finance posts in the past and they were such a great help. Thanks so much for these!

ReplyDeleteOh, good! I love, love, love talking finances and wish it was something that was more acceptable in the general population (feels more like a logic problem to me than an emotional one, which is probably why I feel comfortable with it). Just so glad to have people to discuss it with and bounce ideas around.

DeleteLove the budget posts! And yes - look into pet insurance. Definitely worth it if something comes up!

ReplyDeleteThank you so much for this post Rachel! I don't comment often but I just had to say that I loved this post (and all posts finance-related!). It's so interesting to hear what works for other people. After Christmas and a long holiday overseas, I felt like my generally good spending habits had disappeared and I wasn't sure how to get them back on track. I really want to read the Elizabeth Warren book! I love the 50/30/20 idea and I just opened a new account so I can separate my long and short term savings along those lines. It's so much more manageable than tracking everything. I used an app called ixpensit for a while but I hate the idea of having to enter every cup of coffee. It's too much!

ReplyDeleteSome people love tracking everything, but I just hate it! The percentages are much easier for me to work with and help me from getting totally crazy and cheap. : )

DeleteJust want to echo what everyone else is saying and say again THANK YOU for writing this! The way people avoid talking about budgeting in the blogging world...you'd think it was the scarlet letter. I'm just out of college and I have loans to pay back and rent to keep up with each month and just hearing the percentages you work with is enormously helpful. I keep track of all my expenditures on GoogleDocs but I don't set hard limits on each category... I'm thinking now that it would not only be effective, but would make things easier, too.

ReplyDeleteSo glad it's helpful! I honestly think that the percentages revolutionized my budget. Previously I was just agonizing over how much it's fair to spend and feeling like I should be saving everything. And really, if the money is set aside for spending, you should be able to spend it any way you like, guilt free, even if it seems frivolous to everyone else. Spent money is spent money, the way I see it.

DeleteI love hearing about your budget. After you mentioned it last year, I tried to use the card system but it didn't work for me. But it inspired my husband who loves all things spreadsheet to create a spreadsheet for our spending. We now track what we spend by entering our receipts into a spreadsheet & we also used your numbers to help base our own weekly spending (ie. restaurants, groceries, etc.). We've now stuck with it for over 6 months & I finally feel like I can see where our money is going. Before this, I had no clue. So I have to thank you for your inspiration & help!! Thank you!!!

ReplyDeleteYay! So glad you found something that worked for you!

Deleteit is so, so refreshening and heartening to read your posts about budgeting and finances. it seems to me that few people who aren't finance/econ professionals talk about these things, and it's seriously lacking in (my) real-life conversations between peers. of course, i don't know you at all, but it is incredibly encouraging to read your thoughts on this stuff, and see how other people are managing their money in somewhat similar life circumstances. i have been using mint for years, in part because i had used quicken for almost 10 years before mint rolled out and was familiar with that kind of budgeting and tracking. i definitely have my issues with the service (it can be buggy sometimes, and the customer support leaves something to be desired at times), but now i am in bed with it, so to speak, because six years of my budgets and spending are inside of mint with no way (that i'm aware of) to export them. still, i like the way the budgeting works on that site, and i appreciate the infinite ways i can slice and dice the data there to see where i am now v. where i was a few years ago, financially speaking. sorry, that was a bit of a tangent. at any rate, our posts on this are great, and at the moment it is particularly helpful for me to read your thoughts on managing a joint household budget, as my husband and i are trying to figure out how to make ourselves more comfortable and "okay" with the ways we share funds. thanks, rachel. you're awesome!

ReplyDeleteI do wish more people talked about budgets! I'm never sure if it means they just like to keep them private, or if it means almost no one is budgeting. I love hearing from you guys on these posts!

DeleteI wish more bloggers talked about budget in the detail you do! I don't even love budget details because I am numbers-challenged but you present it in a way that is approachable and understandable. Honestly, it's also comforting to know that there is someone else out there who is the same age as me and isn't in a position to buy a house, so I really appreciate your honesty.

ReplyDeleteI don't love doing cent by cent budgeting, which is why I can't handle systems that make me enter exact amounts. The cards work well for me partly because I can round up and down and it's less effort. (I think I would go to exact amounts if I had an app that made it super easy, but I have zero interest in manually tracking pennies)

DeleteGlad you find it useful!

I love mint but the app can be buggy for me. Just saw this and thought of your cards: https://levelmoney.com/

ReplyDelete